Kenya, Africa’s proverbial Silicon Savanna is about to experience another shakeup affecting digital service providers. Technology startups, betting services, e-commerce players and businesses that purvey services via digital mediums are about to face a potentially disruptive tax increase through the Finance Bill 2024.

The raft of amendments looks to abandon the 1.5% Digital Services Tax (DST) introduced just 3 years ago and in its place introduce a heftier, 30%, Significant Economic Presence Tax (SEPT) on certain non-resident digital businesses deriving income from the Kenyan market.

For those digital operators domiciled in Kenya, their tax obligations stand to quadruple from a current 5% to 20% under the proposed Finance Act 2024.

Policy analysts have questioned the sustainability and wit of such steep and numerous tax increments to an effective 6% after just three years of the DST coming into play. “The taxable profit of a person liable to pay the tax shall be deemed to be 20.0% of gross turnover after which the tax is slapped at 30.0%. Coming from 1.5% DST to what is a 6.0% effective rate is quite steep I think” said Julians Amboko a financial analyst. Analysts have raised concerns about the unpredictable tax policies that could undermine Kenya’s growing state as a regional tech and startup hub.

Alongside targeting non-resident and resident digital service providers, the proposed legislation would raise excise duties on critical enabling services like telephone, internet data, mobile money transfers, and remittance fees from the current 15% up to 20%.

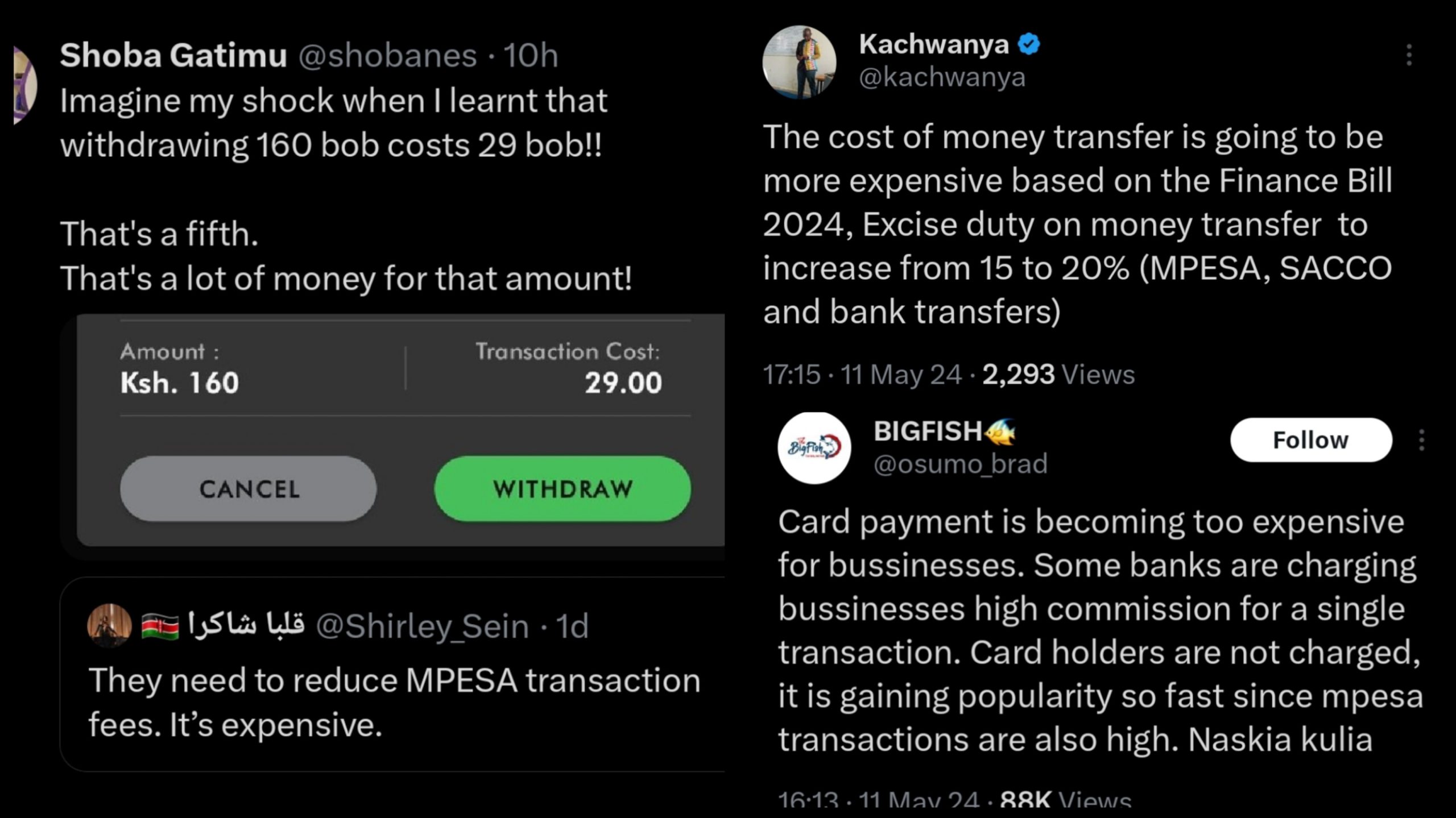

MPESA, Gambling and Banking To Be Affected By The Proposed Finance Bill 2024

Mobile money services such as MPESA are bound to get even more expensive if the proposal to raise excise duties on critical enabling services like telephone, internet data, mobile money transfers, and remittance fees from the current 15% up to 20% is approved.

There has been a growing sentiment that the costs of using the ubiquitous MPESA money transfer service are already quite high, having been affected by previous increases, with a lot of the users hoping for a reduction in costs or looking for alternatives.

Safaricom, the operator of M-Pesa, recently released its annual earnings with a reported 3.5% rise in its annual core earnings to 94.9 billion Kenyan shillings ($724 million) partly driven by the growth of M-Pesa mobile financial services business to 8.8% to 117.2 billion shillings.

With over 83.9 percent of Kenya’s youth engaged in gambling or betting activities according to Geopol, the doubling of excise duty on betting activities from 10% to 20% under the Finance Bill will have huge ramifications. Rapid digitalization has triggered explosive growth in the online gambling sector.

The digital economy and infrastructure in Kenya have allowed millions of Kenyans to leapfrog traditional banking services and access digital economies such as online gambling and mobile money services. The excise tax rates could potentially put a damper on the further growth of these sectors by raising costs for both businesses and users.

Safaricoms’ popular M-Pesa currently has over 30 million subscribers and facilitates billions of dollars in payments across the Kenyan economy. Loan disbursements and repayments, transaction payments, remittances and person-to-person transfers of funds could all potentially be affected by the increased M-Pesa charges and become a burden to low-income users.

The tax measures also propose to remove long-standing VAT exemptions on a wide range of banking and financial services such as loans, account management, and cross-border payments – potentially raising costs across the banking sector.

Finance Bill 2024 to Change Kenya Data Privacy Law

Some of the proposed measures in the Finance Bill aim to give the Kenya Revenue Authority access to personal data. Granting enhanced data monitoring and sharing powers to the Kenya Revenue Authority (KRA) has raised privacy alarms, with experts cautioning on unrestricted and unmonitored access. The proposal aims to exempt KRA from the provisions of the Kenya Data Protection Act when accessing personal information deemed “necessary” for tax assessment and collection.

While KRA states that the goal is purely meant to enhance tax compliance and close loopholes, digital rights advocates have forewarned that unchecked powers could unsettle the entrepreneurial risk appetite for innovation in Kenya.

Another key provision would allow KRA to require any business to directly integrate its operational systems with the agency’s electronic tax system known as eTIMS. Failure to comply would attract penalties of up to 2 million Kenyan shillings ($16,000) per month – a potentially existential threat for smaller startups.

The integrations are aimed at giving the tax authority access to granular, real-time, data on commercial transactions from the business.

These new policies have been driven by the requirement to comply with the IMF’s three-year program under the nation’s $4.43 billion extended loan facility, which views mobile internet, digital platforms, gambling and novel financial technologies as being undertaxed.

Attempting to reduce the tax gap by creating short term tax-receipts from the nascent tech and innovation centres could inadvertently kill future growth. Business leaders are concerned that these measures could kill the proverbial goose that lays golden eggs. They have advised that a stable, fair, tax environment is crucial to nurturing long-term innovation.

As a regional beacon and bright sport for mobile money, e-commerce, fintech, online betting and startup investment, Kenya finds itself battling regulatory and taxation headwinds that if not carefully balanced could erode entrepreneurship that drives technological transformation.

{kind=link}