The Kenyan e-commerce market keeps on growing by leaps and bounds. This has been further fueled by the 90.4% mobile penetration rate that roughly translates to 41 million people. The variety of e-commerce platforms keeps on growing and this could even get better as the number of internet users keeps on soaring annually.

The Kenyan e-commerce market keeps on growing by leaps and bounds. This has been further fueled by the 90.4% mobile penetration rate that roughly translates to 41 million people. The variety of e-commerce platforms keeps on growing and this could even get better as the number of internet users keeps on soaring annually.

The most popular e-commerce model in Kenya is Business to Consumer (B2C), where users directly access the product online and purchase it. My area of interest has been to examine the use of credit/debit/prepaid cards as a mode of payment on these platforms, given that there are other options to choose from such as mobile money and Cash on Delivery.

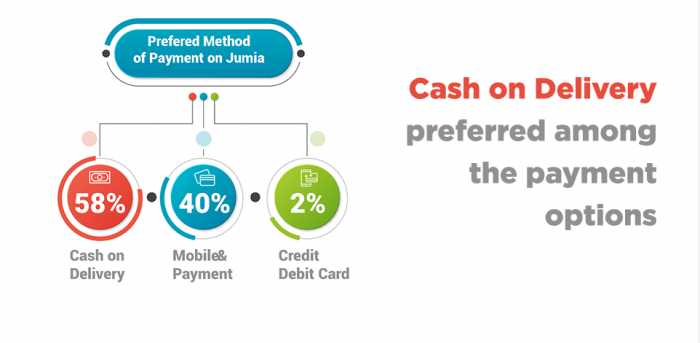

Mobile money continues to dominate as the most preferred choice of payment among the online shoppers. This was evidenced by the growth of MPESA transactions in 2017 with a 8.8% increase from the previous year. The Central Bank of Kenya reports that the value of card payments dropped from Sh.1.39 trillion in 2016 to Sh 1.38 trillion in 2017. In their Mobile report this year, Jumia reported that Cash on Delivery is the preferred mode of payment on their platform.

This could be a paradox of sorts because, while mobile money is king in Kenya, conventional alternative payments such as card payments shouldn’t be declining. This year Safaricom partnered with PayPal to integrate sending of funds between the two platforms. This move could even injure the plastic money model further. So what makes online card transactions so unpopular?

Inconsistencies

The card experience has been marred with a lot of inconsistencies. An infamous tale is told about the Nakumatt Global Card that caused a lot of hue and cry with its users. This was a partnership in conjunction with Diamond Trust Bank. In its heyday, it was used as a pre-paid debit card to speed up buying of goods from online stores. But trouble started soon after some users were suspended from their merchant/seller accounts due to the inability of the card to follow through with payment to other merchants, yet money had been deducted from the card. Cases of money being deducted without a proper reason also came up. Such cases have made it even more difficult to use plastic money for online purposes.

Distrust

This has been a huge hindrance to the developing of e-commerce in emerging markets. A study by Purity Kabuba on the performance of businesses online revealed that customers are likely to distrust a product they have not seen or touched physically. The lack of trust boils down to other aspects such as the safety of personal data which also makes customers jittery about plastic money.

Finally, there is a general lack of trust in using plastic money for online businesses. International platforms have introduced a full money back guarantee on all items to improve the trust levels. Locally, e-commerce players are yet to fully implement this, even as a guarantee on selected items has been introduced but the refund policies still seem to be a tad too difficult.

If the current trend is anything to go by, card transactions will continue being unpopular

To put this into context, I ran a poll on twitter to find out if people would be willing to add credit/debit card information to a Kenyan e-commerce website. This would mean that the card would be used for subsequent transactions. The votes showed that out of 35 people 86% (30) people said they would not dare add their information. The reasons given were as follows.

- There were no reviews about the e-commerce site from other people.

- There was a general lack of trust in anything ‘Kenyan’ as the fear was that mediocrity would play out eventually just like other sectors.

- Why would they use their cards when there was M-Pesa?

Clearly, there isn’t motivation that has been given by local financial institutions on the need to strengthen plastic money transactions. Incidents of local taxi companies deducting money from credit/debit cards of their users, yet they have not used the service continues to add salt to the injury.

The e-commerce players seem not to be doing enough to strengthen trust levels in plastic money transactions, yet they offer one of the best if not security features for shopping online. Local players have been made so comfortable with mobile money to the extent that while other alternatives are offered, no incentives are made on how to strengthen them.

If the current trend is anything to go by, card transactions will continue being unpopular and companies will see no need in having them as a means of payment but rather a conventional payment that is availed on e-commerce sites.

{kind=link}