Are you good with your money? Good for you, you are an anomaly.

The numbers reveal that thousands of Kenyans are listed by the CRB for as little as KES 200 in defaulted loans. A good chunk of us carry more than KES 200K in HELB debt. That is a substantial amount of money. And the country, for context, owes KES 7 trillion to local and international lenders.

That is so much money you could buy all the chicken wings ever.

And, there are thousands of people out here who owe a lot of money to online digital lenders.

But how did we get here?

Unregulated online lending

Digital lenders have been here for a long time now.

They are popular in the country because of one primary thing: M-PESA, which means that customers can receive instant loans.

However, the online lending space has been chaotic at best, which is why tens of loan apps have mushroomed with the worst services ever known to man.

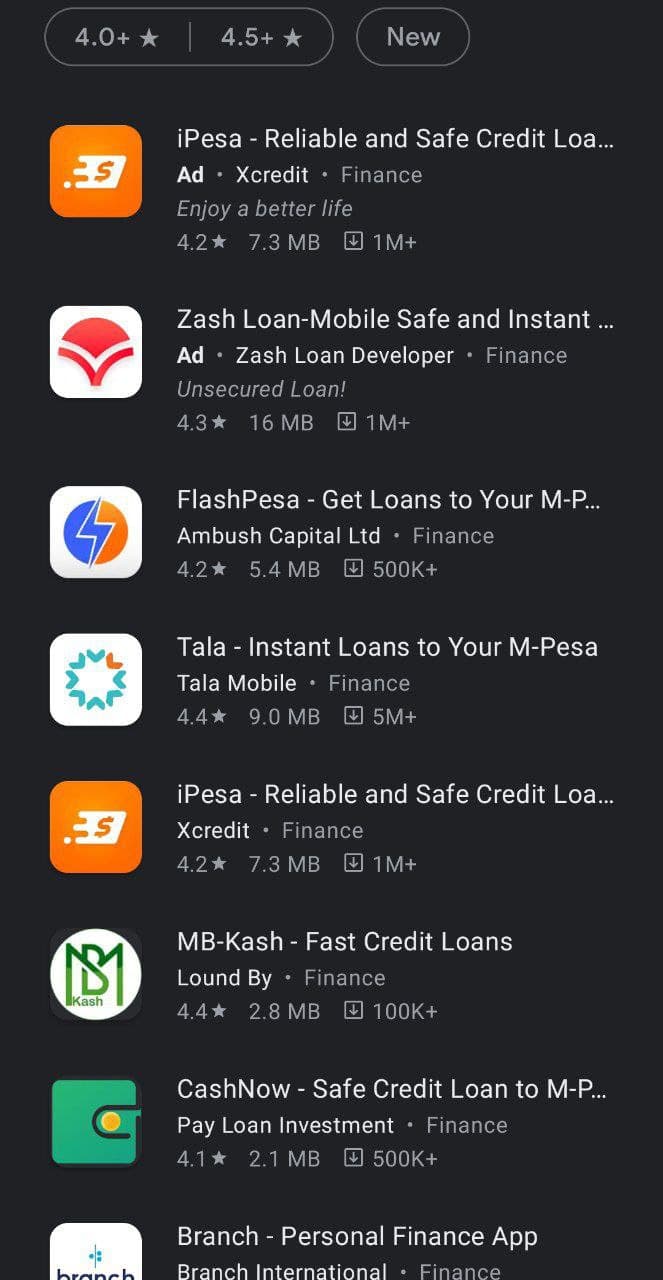

A quick ‘loans’ search on Google Play Store should give you the depth of these issues: there are so many companies that run the apps.

And before we proceed, it should be noted that not all these apps are bad per se: some have attempted to adhere to safe and ethical practices, including Branch and Tala. Other mobile lending products such as Timiza are hardly predatory because they are associated with banks (ABSA), which fall under the scrutiny of CBK.

It is obvious that the majority of these apps are shylocks masquerading as online lenders.

Worse, is that they have been given a platform to reach out to more customers, customers who, through no fault of their own, have fallen prey of the apps’ unethical practices, and have since found themselves in a debt pit with slippery walls.

A bill is coming

For now, the CBK and Parliament are pursuing a government-backed bill named the CBK (Amendment) Bill, 2021.

On the whole, the Bill seeks to introduce some sanity into online lending by:

- Auditing the companies

- Making sure that online lenders are under the same regulatory umbrella as banks

- Regulating their interest rates to a reasonable rate

- Making sure the lenders have a local physical office

- Making sure that lenders don’t abuse your private data

The insanity of online lenders

With that in mind, let’s break it down how these apps have been, quite literally, insane in the manner they run their business.

Why are they too many? Well, because the space is lucrative and unregulated so, every one is joining the party to mint as much money as possible from Kenyans who have a proven record about their insatiable appetite for loans. Their numbers also give Kenyans options, which means that if they get rejected by one app, the next one will likely receive them with open arms.

Say one app is willing to hear you out. The amount of information you would give up is outrageous. The apps would ask you full name, ID, place of residence, where you work, your work address, two guarantors, your entire phone book, an image of you, and more. While the loans are unsecured (we all know that), this amount of personal information on their side is just dangerous. But do Kenyans really care?

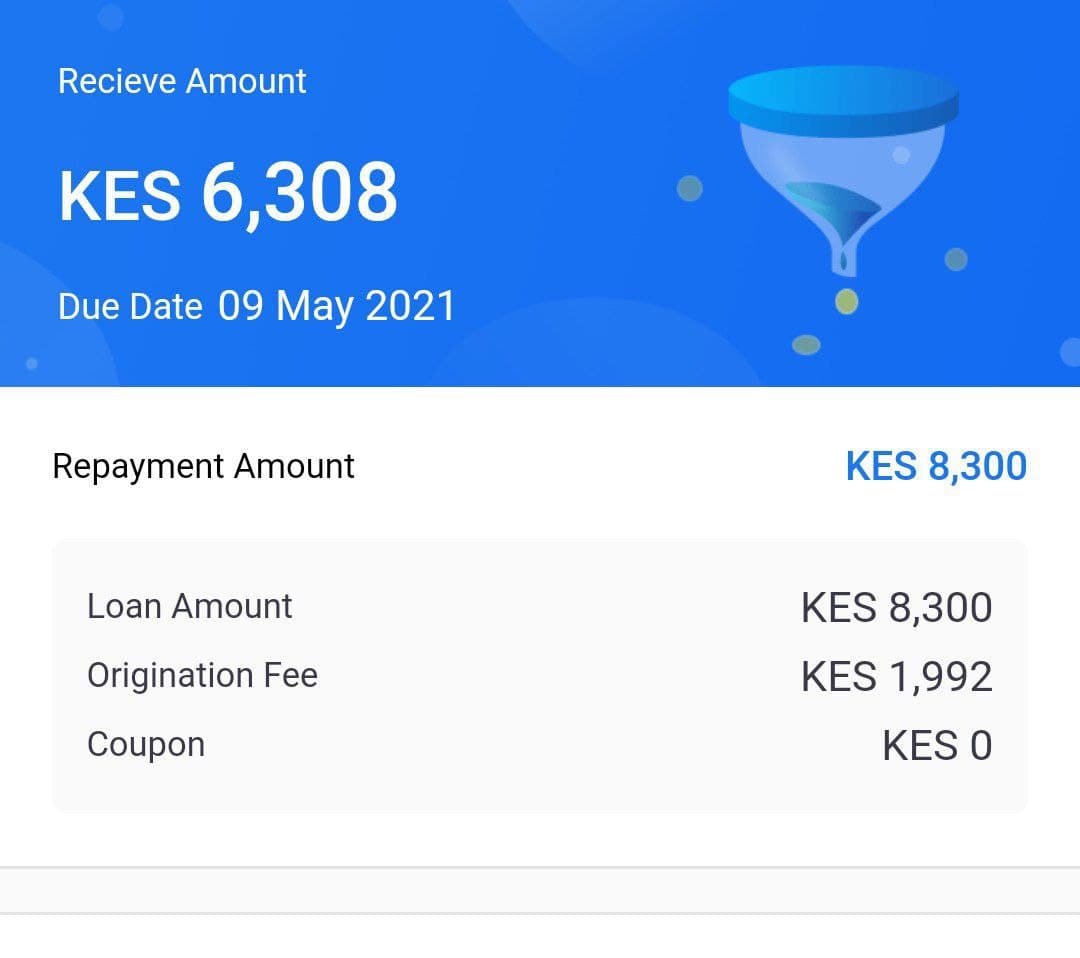

The apps then do their thing in the background and give you a limit. If you qualify for say KES 500, they will disburse KES 375 or thereabouts to your M-PESA. Worse cases exist, because as you borrow and repay on time, the limit increases, with even worse interest rates. You don’t believe me? Check this out!

You have received the money, yaay! But are you aware that the company will want it back in two weeks? Two weeks. That should explain itself.

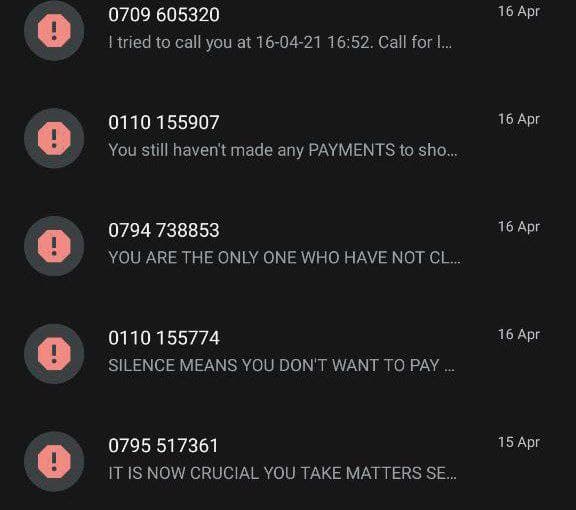

Now, let’s go the part where the apps harass you:

- They are going to spam you with tons of text messages even when your repayment period hasn’t arrived.

- Then, they are going to call you before the repayment day, as if you’d forget you owe them money.

- In other cases, an army of two or three guys would be on your neck one day before the repayment day. These people would tell you scandalous stories, that they are likely to increase your limit if you pay on time, or that you are supposed to repay your loan ONE day before the deadline (even when their apps say otherwise).

- On the D-day, a ton of threatening and passive-aggressive messages would stream into your phone the whole day.

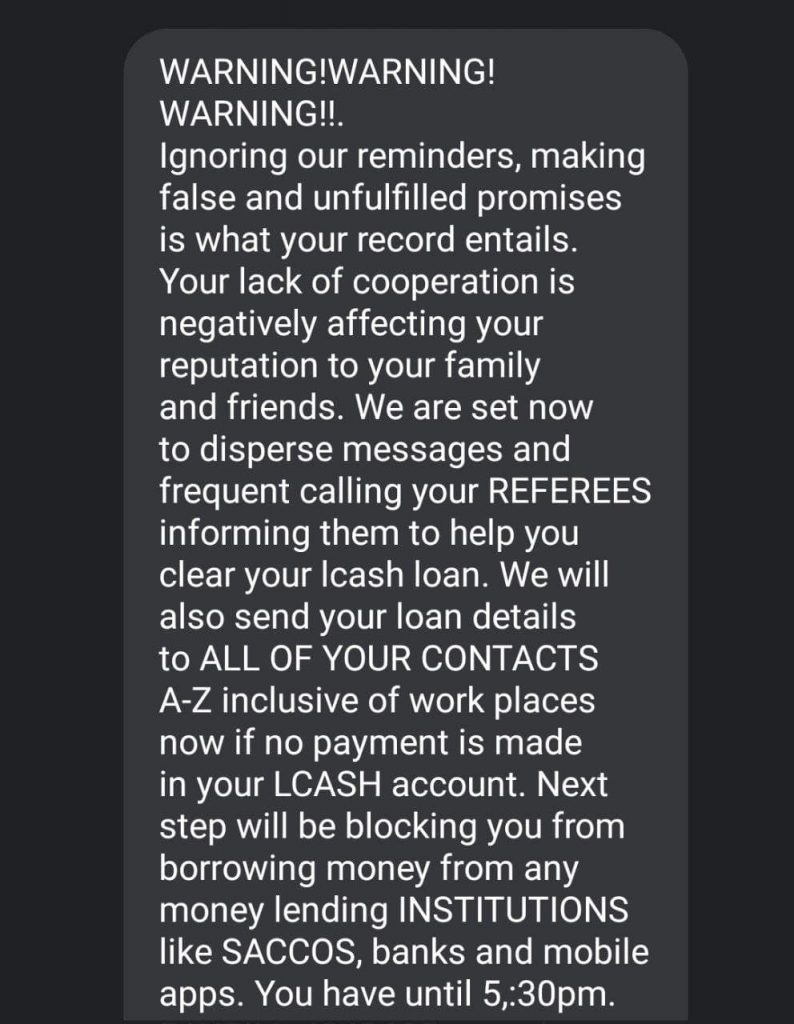

- Worse is if your loan rolls over to the following day, and that is when you are going to see their true side. You would be threatened about them calling any person from your list ‘so they can help your clear your loan.’ Or outrightly shame you about texting your phone book list about your balance. I mean, that has to be illegal and wrong in 1000 ways. And you think they don’t do that? Your answer is as good as mine.

- If you prove stubborn, they would source the services of their most brutal loan collector who, as reports tell us, would even abuse you for playing with their money.

- Do you also know that they fine you for every day you don’t clear your loan?

It should be remembered that these apps are here, and give you money because they don’t check if you are a defaulter at the CRB. The loans are just that insecure, which increases their risk that also extends to the borrower.

We hope that the aforementioned bill kicks out these borrowers and that if you have been affected, then you can learn to be careful next time and save yourself trouble later.

{kind=link}