The Kenyan mobile app and the overall African mobile app market has shown significant growth propelled by a growing fintech space, a rise in ‘super apps’, and the COVID-19 pandemic amongst other factors.

This is according to a new report by AppsFlyer, a global marketing measurement leader in partnership with Google.

In order to understand the effect of these first lockdown measures on mobile, they compared activity in Q1 2020, before the restrictions, with Q2 2020.

Analysis of over 6,000 apps and 2 billion installs across South Africa, Nigeria, and Kenya, between Q1 2020 and Q1 2021, the report found that the African mobile app market showed strong growth, with overall installs increasing by 41%. Nigeria showed the highest growth, with a 43% uplift, followed by 37% in South Africa, and 29% in Kenya.

With people spending more time at home, it’s not surprising to see overall app installs increase by 20%. On a country level, South Africans were quick to take to their mobile devices as the first lockdown hit, with installs increasing by 17%. The situation was more muted in Nigeria and Kenya, with increases of 2% and 9% respectively. These differences are likely due to the varying levels of restrictions exercised by the three countries, with South Africa facing the strictest.

33% of 2020’s in-app purchasing revenue was generated in Q3, as consumer spending grows

Showing perhaps the biggest trend, in-app purchasing revenue numbers soared between July and September, with a 136% increase compared to the previous three months. This accounted for a third of the year’s total revenue, highlighting just how much African consumers were spending within apps, from retail purchases to gaming upgrades.

South Africa’s in-app purchasing revenue surged by a massive 213%, with Nigeria and Kenya also showing significant increases of 141% and 74% in the same time frame.

South Africa and Nigeria saw year-on-year growth in finance app installs by 116% and 60% respectively, as the need to reduce social contact has led to even more users adopting digital solutions for their financial needs.

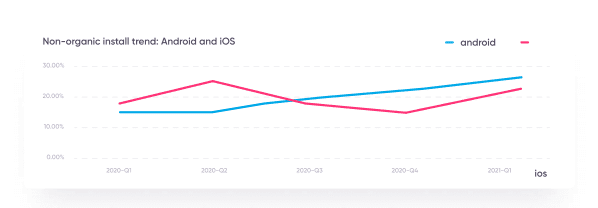

Android’s larger market share within Sub-Saharan Africa has seen advertisers spend more budget on the platform. Non-organic installs increased by 54%, compared to 19% for iOS.

The cost per install (CPI) on iOS also increased by 21% between Q2 and Q3 2020, which meant iOS app developers were getting fewer installs for the same budget. Towards the end of the year and into 2021, there was no uplift in non-organic installs on iOS compared to 40% on Android.

The report found similar levels of overall growth across verticals during the year, with gaming installs increasing by 44% and non-gaming increasing by 40%.

The first set of restrictions in March 2020 had a huge impact on downloads of gaming apps, which increased by 50% in Q2 2020 compared to Q1, compared to non-gaming apps which only increased by 8%.

Africa has one of the fastest in the world, making the African app market primed for success now and into the future. Here are some of the other trends that are impacting the state of mobile in the continent.

Nimble start-up apps finding their feet in the African market

Start-up culture is prominent across a diverse range of industries in Africa, and the app market is no exception. Nigeria leads the way in terms of the volume of startups, while South African companies, home to an established venture capital network, raked in the highest amount of funding in 2020.

Not only is entrepreneurship thriving across the continent, but these start-up apps — unburdened by legacy infrastructure of technology — were able to navigate and respond to the challenges presented by the pandemic.

For example, as new consumer needs emerged, particularly around remote access to services, nimble apps were able to respond and adapt quickly to meet customer expectations during challenging times. This included launching new products, rethinking business models and revenue streams, or partnering with other organisations.

Fintech apps fill a huge need in society

Africa combines a mobile-first population with large sections of society who are inadequately served by traditional financial institutions; those unable to open bank accounts, or face other barriers that prevent them from accessing financial services.

This has opened the door for agile fintech and finance apps to provide services that have been readily adopted by the African market, with investment growing significantly in the sector in 2020.

The COVID pandemic has led to even further growth as the need to reduce social contact has led to even more users adopting digital solutions for their financial needs. South Africa and Nigeria saw year-on-year growth in finance app installs by 116% and 60% respectively.

The rise of super apps

Super apps are on the rise in Africa; “all-in-one” apps that offer users a range of functions such as banking, messaging, shopping, and ride-hailing. It’s a model that emerged in Asia in the shape of apps like WeChat and Alipay, and has now

taken root in Africa.

To an extent, the rise of super apps in Africa owes much to the same conditions that have led to a surge in fintech apps: systemic underbanking across the continent. Super apps remove some of the barriers that these users face, as well as

providing a level of customer insight and experience that traditional banks cannot.

Device limitations are also a factor in Africa. For users whose smartphones can only store a limited number of apps, they will be naturally drawn to apps that can fulfil a wide variety of lifestyle functions.

Data and connectivity challenges

Although the African app market has grown significantly, the continent’s population still faces challenges over connectivity. At the end of 2019, before the start of the COVID-19 pandemic, mobile internet adoption in Sub-Saharan Africa stood at 26% — significantly below the global average of 49%.

This naturally presents challenges to user acquisition and retention, with data showing that only 12% of consumers open an installed app after 3 days. Again, this is a contributing factor to the rise of super apps. The apps that provide the most value to users (through a multiservice offering) are more likely to be retained on their devices.

“Like the global app market as a whole, mobile in Africa saw significant growth in 2020 that carried forward into 2021. Installs — especially non-organic installs, driven by marketing activities – grew by a large margin, with the COVID-19 pandemic accelerating the trend even further. As Africans spent more time with their smartphones, they were increasingly likely to spend money in apps, indicating just how important mobile can be for driving revenue,” said Daniel Junowicz, RVP EMEA & Strategic Projects, AppsFlyer.

“These trends are only going to continue, and being able to make data-driven decisions about what campaigns are working and where to invest money will be key for any marketer looking to succeed in this thriving landscape,” adds Daniel.

“While mobile in Africa grows, it remains a for marketers and developers. Agile startups, such as those in the fintech sector, have been able to thrive amid unprecedented conditions, and even compete with all-in-one super

apps that are traditionally dominant on African mobile devices. These opportunities will only expand further as mobile connectivity improves in the coming years, ” said Rama Afullo, Apps Lead for Africa, Google.

The full report can be accessed here.

{kind=link}