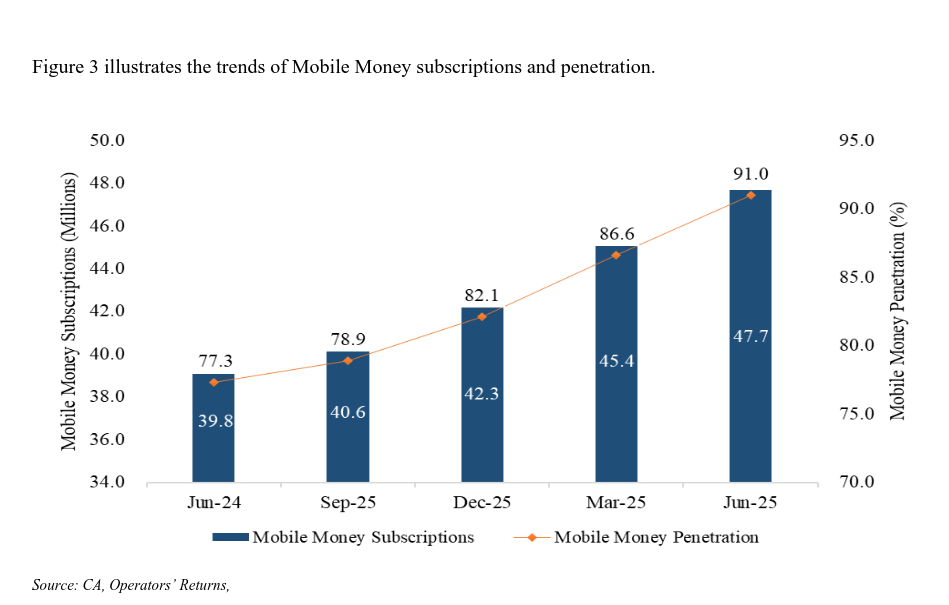

Kenya’s mobile money sector has reached a major milestone, with the latest Communications Authority (CA) data showing 47.7 million active subscriptions as of June 2025.

This translates to a penetration rate of 91%, up sharply from 77.3% in June 2024, indicating mobile money’s dominance in financial services and its central role in driving financial inclusion.

The surge in subscriptions highlights how mobile money has evolved from a simple transfer service to a core financial infrastructure in Kenya.

READ: Kenya Hits 45 Million Mobile Money Users With M-Pesa in the Lead

With nearly every adult Kenyan now connected to a mobile wallet, the sector has become indispensable for households, businesses, and even government transactions.

Market Breakdown

The CA report indicates that Kenya’s 76.7 million SIM subscriptions as of June 2025 represent a 146.3% penetration rate, a sign of multiple SIM ownership and widespread connectivity.

Of these, mobile money subscriptions stood at 47.7 million, showing that nine out of ten mobile users are actively using financial services linked to their mobile numbers.

This rapid adoption has been fueled by the expansion of telecom infrastructure, increased smartphone penetration, and the demand for mobile broadband, mobile money, and mobile banking services.

Safaricom Still Leading But Rivals Are Expanding

Safaricom’s M-PESA remains the dominant player, but Airtel Money and Telkom’s T-Kash are steadily growing their footprint.

As competition heats up, customers are benefiting from reduced transaction costs, better interoperability, and an expanding range of digital financial services.

Rise of Mobile Money Places Banks on Alert

With mobile money now accounting for a significant share of mobile revenues, traditional banks are under pressure. The ease, affordability, and accessibility of mobile wallets threaten to erode banking market share in deposits, payments, and even lending.

For regulators, the challenge lies in balancing growth with stability.

Issues such as consumer protection, anti-money laundering measures, transaction limits, and cross-border payments are becoming increasingly critical as mobile money scales to near-universal penetration.

READ: Card Usage Drops as Mobile Payments Rise

The coming years will test how well banks, fintechs, and regulators can adapt. With 47.7 million subscriptions already active, the market is approaching saturation, meaning growth will likely shift from user acquisition to service diversification and innovation.

{kind=link}