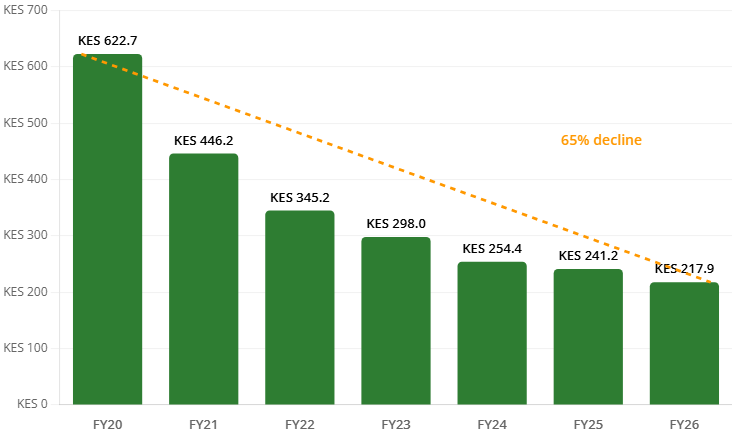

In the past 7 years, the average amount Kenyans borrow from Fuliza has decreased by KES 404.8, which represents a 65% reduction. According to Safaricom, the average amount borrowed by Kenyans (ticket size) was KES 622.7 in FY20 and dropped to KES 217.9 in FY26.

This borrowing pattern indicates an economic environment where total personal credit is shrinking and strained household cash flows.

Fuliza is a key indicator of strained household cash flow. Safaricom describes this lending platform as “a product that enables customers to access an unsecured line of credit by overdrawing on M-Pesa to cover short-term cash-flow shortfalls.”

Since it was launched in 2019, the average amount M-Pesa users borrow from the platform has consistently declined.

This decline is happening even though some users recently had their Fuliza limits increased. It reflects the economic gap in the country, where only a small number of people have extra income to spend.

Fuliza Borrowing Indicates Biting Poverty

Over the past 3 years, average borrowing has been under KES 300. This aligns with findings from the Institute of Public Finance, which reports that nearly half of Kenya’s population lives below the poverty line, with over 23 million citizens unable to spend more than KES 387 (~$3) per day.

READ: M-Pesa Visa Users Surge 62%, But Customer Spending Drops

“Real average wage earnings per employee have dropped by 4% in the private and public sectors over 2022-2024, meaning a decline in purchasing power,” the report stated.

This finding is supported by a Kenyan Poverty Report from the Kenya National Bureau of Statistics (KNBS). The KNBS poverty report states that 39.8% of the population lives below the overall national poverty line.

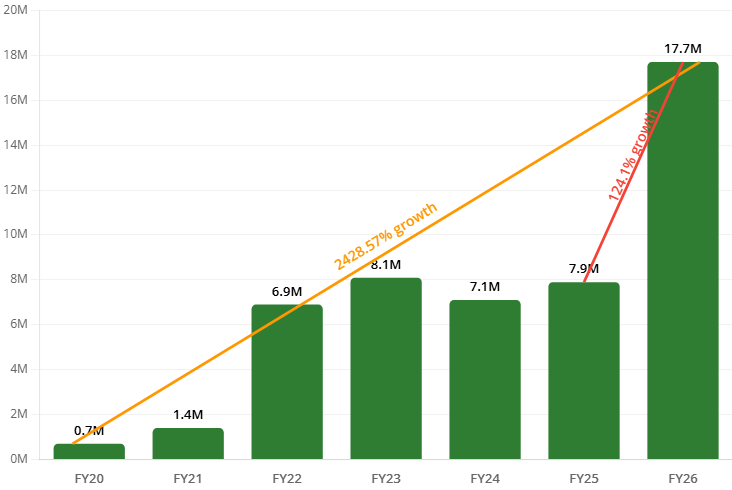

More Kenyans now have to rely on small loans to cover perennial short-term cash flow deficits. As a result, Fuliza, an opt-in platform, has grown its user base 25.3 times in just 7 years.

At 0.7 million users in FY20, it has grown by 2,428.57% to reach 17.7 million users in FY26. This need for short-term credit spiked by 124.05%, adding 9.8 million users to the overdraft platform in just one year.

About 44% of M-Pesa’s 40 million users have opted into Fuliza, up from 19.75% the previous year.

Even with smaller disbursements, more users have meant the total amount disbursed has kept growing. In FY26, the platform disbursed KES 1.47 trillion, its highest amount ever.

READ: How to Opt Out of Fuliza

For Safaricom and its partners, NCBA, KCB, and Sidian Bank, Kenyans’ dependence on credit means profit. Fuliza earned KES 6 billion in revenue in FY26.

This is three times more than what M-Shwari, Safaricom’s second-largest lending platform by revenue, earned in the same period, which was KES 1.9 billion.

President Ruto’s Tax Policies

President William Ruto’s administration has played a part in the strained pockets. Since coming into office, Ruto has introduced a combination of new statutory deductions.

Two of these have been unsuccessfully challenged in court. These are the 1.5% Affordable Housing Levy and the 2.75% uncapped Social Health Insurance Fund (SHIF) deduction. President Ruto has also increased contributions to the National Social Security Fund (NSSF).

Fuel and food prices increased after subsidies were removed and the road maintenance levy was raised to KES 25 per litre. The levy was KES 18 before 2022, and it was increased by KES 7 in July 2024.

Additionally, Ruto’s first finance bill raised the top PAYE rate for high earners to 35%. These tax changes have reduced take-home pay for many Kenyans, pushing more people to microcredit services just to get by.

{kind=link}