Kenya’s automotive market has pulled off a noteworthy recovery in 2025, with new vehicle sales through November already exceeding total sales from the entire previous year.

Dealers moved 12,427 units in the first eleven months of this year, surpassing the 11,352 vehicles sold across all of 2024.

Year-on-year growth from the same January-November period shows sales jumped 22.3%, climbing from 10,160 units in 2024 to the current figure (thanks, BD).

This marks a turnaround after demand had weakened under pressure from expensive credit and government payment delays that left contractors waiting for money.

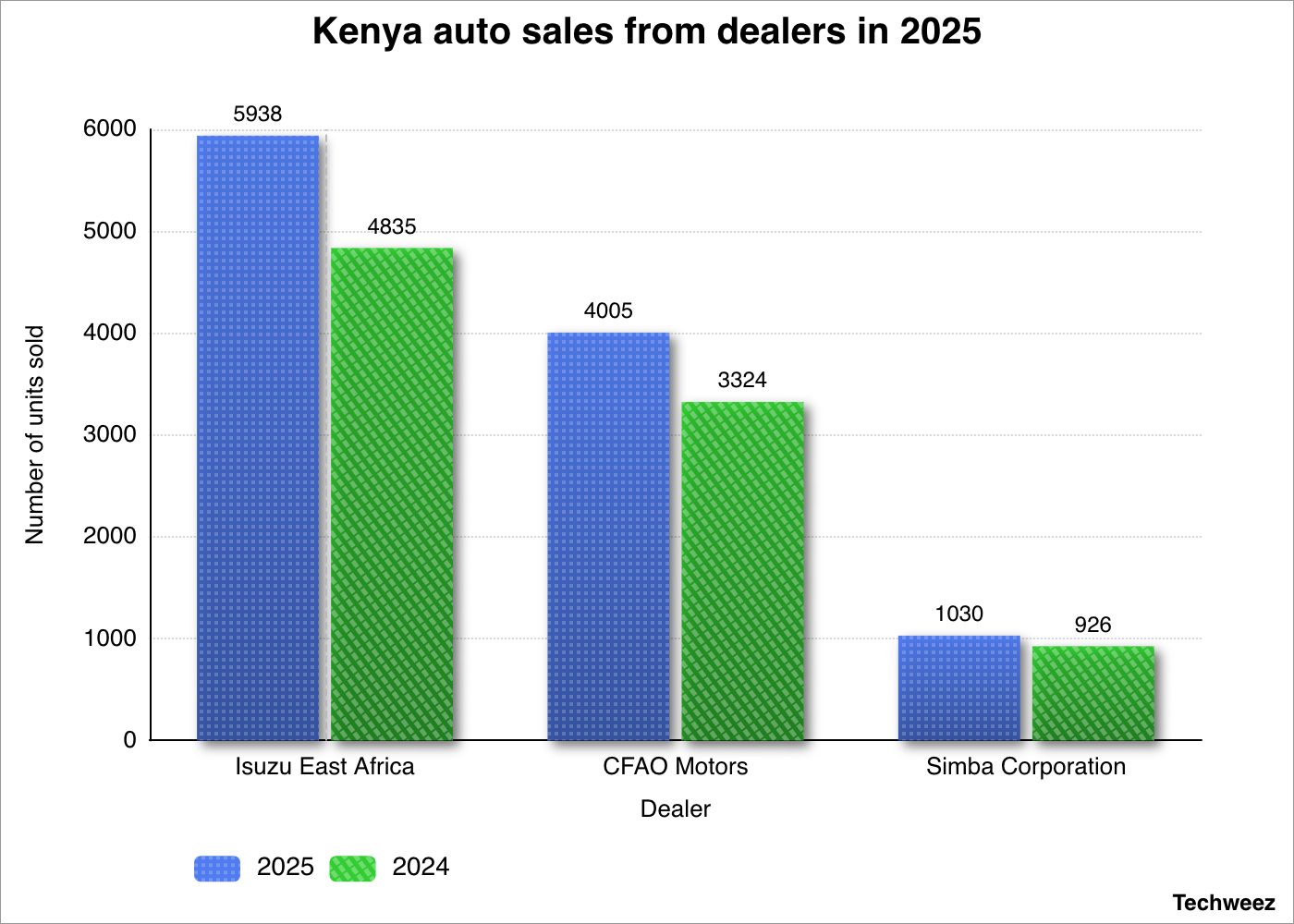

Market leader Isuzu East Africa posted the strongest performance, selling 5,938 units between January and November 2025, up 22.8% from 4,835 units during the same stretch last year.

The company dominates commercial vehicle sales, focusing on pick-ups, buses, trucks and SUVs.

CFAO Motors, which handles multiple brands including Toyota, Mercedes, Volkswagen and Hino, delivered 4,005 units in the review period.

That represents a 20.49% increase over the 3,324 units sold in the corresponding months of 2024, driven by stronger demand for light commercial models.

Simba Corporation, which distributes Mitsubishi, Proton, Ashok Leyland and Mahindra vehicles, recorded sales of 1,030 units compared to 926 units in the prior year period.

The recovery stems largely from falling interest rates. Commercial bank lending rates dropped to 15.07% in September from 16.91% a year earlier and a recent high of 17.22% in November 2024.

The Central Bank of Kenya drove this decline by cutting its benchmark rate from 13% in mid-2024 down to 9% currently.

Cheaper financing has reopened the market for businesses that had frozen vehicle purchases. Companies in construction, utilities, field services, beverage distribution and transport sectors are now replacing aging fleets after sitting on the sidelines during the high-rate environment.

Government contractors who had been waiting for delayed payments have also started receiving funds, freeing up capital for equipment purchases.

The shift in financing costs matters a lot for vehicle buyers. When rates peaked above 17%, the monthly cost of financing a commercial vehicle became prohibitive for many businesses.

The drop to around 15%, combined with CBK’s benchmark sitting at 9%, has made asset financing workable again.

READ: Kenya’s Car Sales Rise 25% as Market Hits Pre-COVID Levels

Dealers have also increased direct engagement with customers this year, organizing events across the country to discuss financing options and ensure vehicles meet operational needs.

This hands-on approach has helped rebuild confidence among buyers who had pulled back from major capital expenditures.

The 9.5% growth over full-year 2024 sales suggests the market has stabilized after its downturn. With one month still remaining in 2025, final figures will likely show even stronger annual performance, reinforcing the view that Kenya’s automotive sector has moved past its recent struggles.

{kind=link}