Safaricom’s FY26 results confirm what many Kenyan traders already know from experience. Pochi La Biashara has grown from a simple M-PESA feature into a key part of how small businesses receive payments across the country.

Total merchants across the two business products, Lipa Na M-PESA and Pochi, grew from 1.8 million to 3.1 million in a single year, a jump of 71.4%.

The real story is in how that growth split between the two products, because it shows Safaricom’s informal-sector bet paying off faster than its formal one.

Merchant Growth: FY ’25 vs. FY ’26

| Metric | FY25 | FY26 | Growth |

| Lipa Na M-PESA merchants (KES Million) | 0.7 | 1.0 | +54.2% |

| Pochi La Biashara merchants (KES Million) | 1.1 | 2.1 | +81.5% |

| Total merchants (KES Million) | 1.8 | 3.1 | +71.4% |

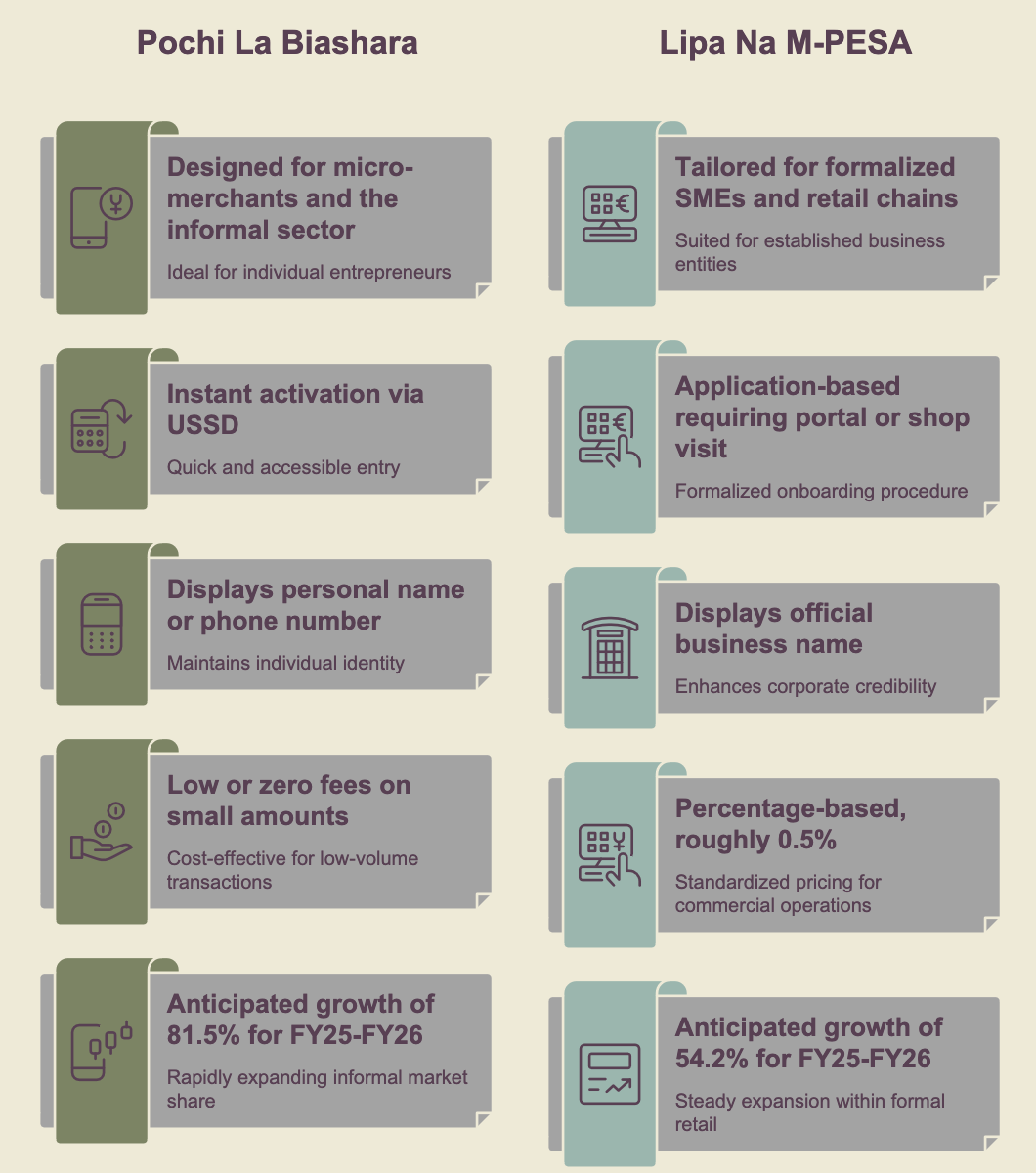

Pochi’s merchant base grew faster than Lipa Na M-PESA’s by a wide margin, and it now accounts for roughly two-thirds of all registered business wallets on the platform.

That is a meaningful shift for a product that was originally pitched as a stopgap for traders too small or too informal to bother with a till number.

Why Pochi Spread So Fast

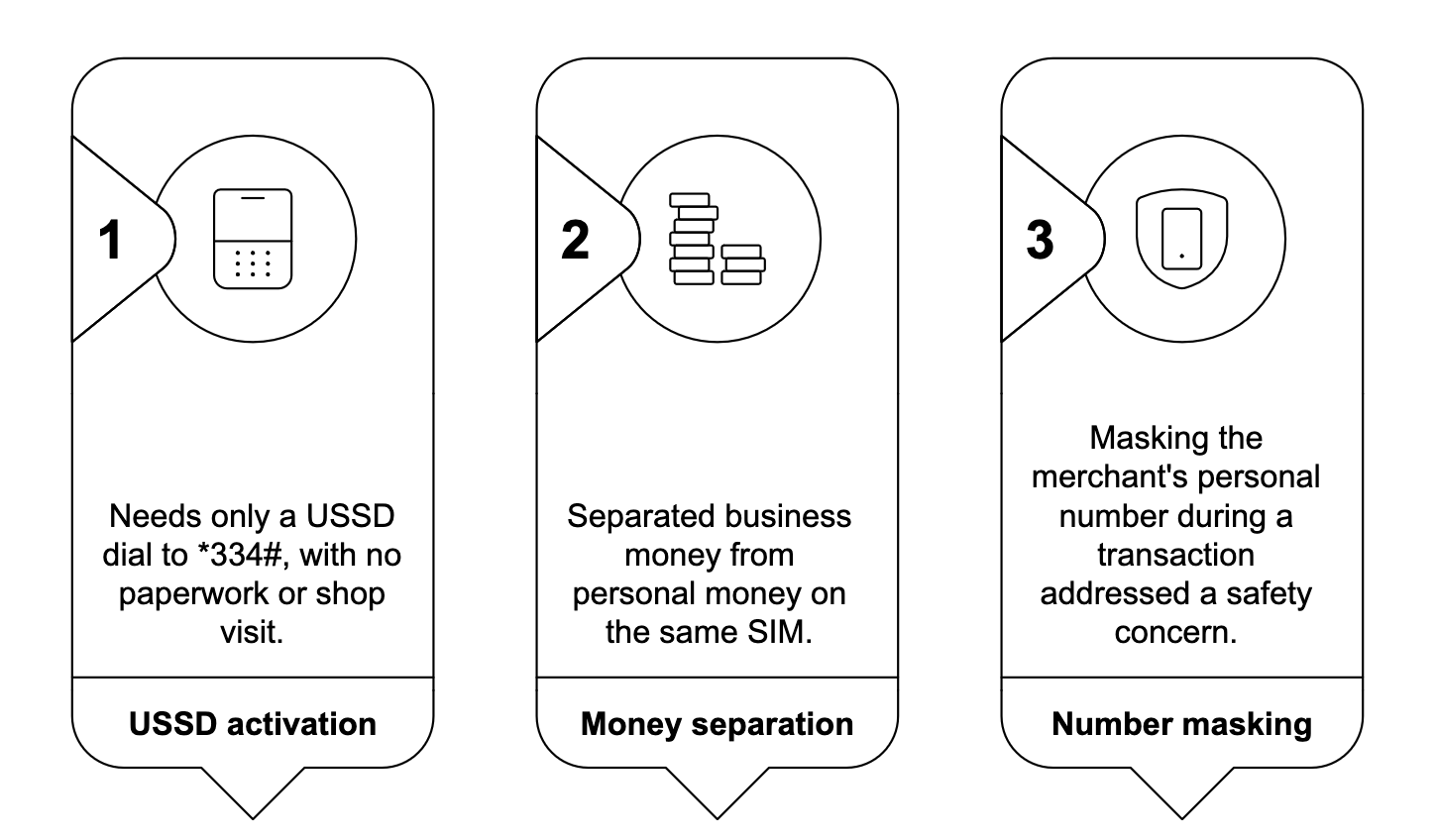

Pochi’s design solved three long-standing problems in Kenya’s informal economy.

The first was the low barrier to entry. Activating Pochi only requires dialing *334#. There is no paperwork, no need to visit a shop, and no waiting period.

This made it accessible to Mama Mboga vendors and boda boda riders who could not justify registering a formal till and needed a business tool that worked just as well on a feature phone as it did on a smartphone.

READ: How M-PESA “Kadogo” Led to 17.1 Billion Free Transactions for Safaricom Users

The second was the mixing of personal and business money on a single SIM, which had long undermined financial discipline among micro-entrepreneurs and made it nearly impossible to build a credible transaction history for lending purposes.

Pochi separated the two without forcing traders to carry a second phone or manage a second account.

The third was privacy. Masking a merchant’s personal number during a transaction removed a real safety concern, especially for women traders who make up a large share of the informal retail sector.

Before this change, many had to share their personal contact details just to receive payments.

Revenue Tells a Clearer Story

Merchant numbers only don’t give the full picture. Revenue growth on Pochi outpaced merchant growth, which points to something beyond adoption.

Merchant Revenue: FY ’25 vs. FY ’26

| Metric | FY25 | FY26 | Growth |

| Lipa Na M-PESA revenue (KES Billion) | 7.6 | 9.3 | +21.7% |

| Pochi revenue (KES Billion) | 2.2 | 4.0 | +86.0% |

| Total merchant revenue (KES Billion) | 9.8 | 13.3 | +35.8% |

Pochi’s revenue grew 86% against merchant growth of 81.5%, meaning each merchant is now pushing more transaction value through the wallet than a year ago.

Traders are not just signing up; they are shifting a larger share of daily cash flow onto the platform, which suggests Pochi has moved from being a convenience to becoming the default way many small businesses collect money.

Lipa Na M-PESA’s merchant count grew by 54.2%, but revenue increased by only 21.7%.

This suggests that many formal SMEs had already digitized most of their collections in previous years, or that growth came from newer merchants processing lower transaction volumes, reducing the average revenue per merchant.

Two Products, One Strategy

Safaricom appears to be taking a practical approach instead of pushing every trader to use the same product.

Lipa Na M-PESA is designed for businesses that want a formal way to accept payments, while Pochi serves the large informal sector that has traditionally relied on cash.

Together they cover nearly the full spectrum of Kenyan commerce, from a supermarket chain down to a single vegetable stall.

The Next Frontier: Turning Pochi Into Collateral

The more consequential shift is what Pochi’s transaction data could become in the hands of banks.

Till Number and PayBill already back credit products like Fuliza Biashara, built on a simple logic where banks track the volume, frequency, and value of a merchant’s incoming payments, then lend against that pattern with automated deductions from future transactions.

The basic idea will be if a loan isn’t repaid, the lender can take what’s owed straight from the borrower’s account. In Pochi’s case, that would mean pulling repayment directly from someone’s M-PESA balance.

It works like traditional collateral such as a car or land, except there’s no physical asset involved. The wallet balance itself becomes the security.

Pochi wasn’t built for this kind of lending, but it’s getting there. Safaricom and Pezesha have launched Taasi Pochi, a credit product based on Pochi transaction history rather than formal business records.

It’s an important first step, showing that everyday wallet activity can be treated as a real basis for lending.

The real challenge isn’t legal but practical. A Pochi wallet is tied to someone’s personal phone line, not a registered business, so banks struggle to separate business income from personal spending or judge if that business will still be active next quarter.

Some fintechs are already solving this. Pezesha’s Patascore tool scores borrowers using transaction patterns instead of physical assets. Closer links between banks and Safaricom’s systems could make this scoring instant.

Whoever solves this verification problem will turn Kenya’s informal economy into a new lending market, where a fruit seller’s cash flow could carry as much weight as a formal business license does today.

The Network Effect That’s Doing the Heavy Lifting

Once enough vendors along a street or in a market accept Pochi, customers start carrying less cash, which then pressures the remaining cash-only traders to sign up simply to avoid losing sales.

That loop is largely what explains the current state of affairs, where a Pochi prompt is now expected at every informal point of sale or service.

GSMA data cited alongside the FY26 results shows that women make up 52% of active Pochi users. This reflects the gender balance in the informal retail sector and suggests the product’s simple design has helped remove some of the barriers that previously kept many women traders relying on cash.

From Payments to a Full Business Platform

The FY26 numbers point toward Pochi evolving past its original job of just collecting payments.

Digitizing years of informal cash flow creates a transaction history, and partners such as Pezesha are already using that data to extend unsecured working capital loans to traders who had no prior access to formal credit.

Safaricom’s Mali investment product is also being layered onto Pochi balances, letting merchants earn interest on money that used to sit idle or get spent immediately.

Micro-insurance and health cover bundled directly into the wallet look like the next logical addition, given how much of the informal sector currently operates with no safety net at all.

READ: Biggest Taxpayers Remain a Small Group of Formal Businesses, KRA Data Shows

Tax integration is likely to be the most sensitive part of this plan. A digital wallet could help informal traders gradually become part of the tax system through voluntary compliance, something the Kenyan government has tried to achieve through other approaches with mixed success.

However, it is also the area where merchants are most likely to push back.

{kind=link}