Kenya’s broadcasting industry is caught between two worlds. Traditional radio and TV still command massive audiences, but the digital shift is catching up.

A new report from Communications Authority tracking media consumption from mid-2024 through 2025 reveals this transition, with some surprising patterns about who consumes what and where advertisers are placing their bets.

Radio and TV Are Still the Dominant Players

About 73% of Kenyans listened to radio in early 2025, matching TV’s reach at the same level. These figures have held remarkably steady over the past year, suggesting that reports of traditional media’s death have been greatly exaggerated.

Quarter after quarter, roughly three-quarters of the population tune in to both mediums.

What’s interesting is that men engage more with both radio and TV than women, a gap that persists across all quarters measured. Radio listenership increases with age, peaking among people 35 and older, who hit 78% engagement rates.

The youngest group surveyed, 15- to 17-year-olds, show the lowest radio interest at 67%.

Geography matters enormously too. Rural areas dominate radio consumption at 77%, compared to 65% in cities. The medium’s affordability explains much of this pattern.

In the lowest income category (*LSM 1 to 4), radio listenership reaches 90%, while the wealthiest segment (LSM 12+) sits at just 63%. When you can’t afford or access TV, radio remains king.

Lower Eastern, Lake, Rift, and Western regions all posted radio listenership above 80%. Meanwhile, North Eastern registered the lowest figures, dropping to 30% in early 2025 after bouncing around 45% previously. Nairobi and North Western also trailed national averages.

Language Distribution on the Airwaves

Swahili dominates radio across Kenya, attracting over 60% of male listeners and 55% of female listeners consistently. Vernacular stations come second, with women showing slightly stronger preference for local languages than men.

English-language radio maintains a small but stable presence, never breaking past 12% of total listenership.

The urban-rural divide shows up clearly in language preferences. Cities show nearly triple the preference for English-language stations compared to rural areas.

READ: Kenya’s Cable TV Market Rebounds with 31.5% Growth

In contrast, vernacular radio thrives in the countryside, where it captures a significantly larger share than in urban centers.

Western and South Nyanza regions show the strongest Swahili preference, with Western hitting 87% in early 2025. Lower Eastern and Lake regions favor vernacular programming, regularly exceeding 57% listenership.

English finds its strongest foothold in Nairobi, where it captures 21-24% of listeners, and North Eastern, though overall numbers remain modest.

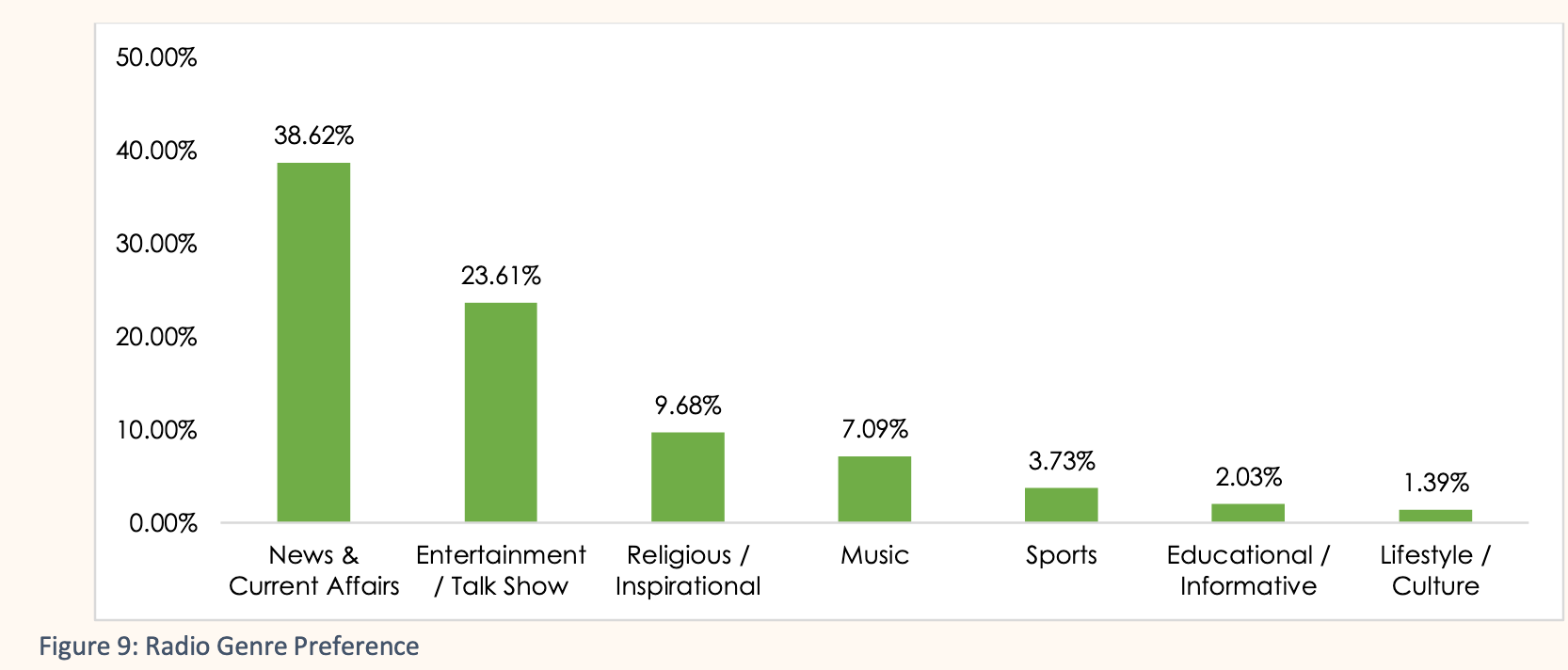

When it comes to content, news and current affairs crush everything else, commanding 38.6% of radio listenership. Entertainment and talk shows come second at 23.6%, followed distantly by religious content at 9.7% and music at 7%.

TV’s Urban Advantage

TV viewership mirrors radio’s 73% national reach, but the demographic patterns differ. Unlike radio, TV viewership actually declines among the oldest viewers and shows troubling drops among young adults.

The 18-24 age group fell from 80% viewership to 72% in early 2025, suggesting broadcasters are failing to hold younger audiences.

Urban areas dominate TV consumption, consistently recording figures above 80% compared to rural levels around 73%. The income gap is even more dramatic than with radio.

READ: TVs and Fridges Now Top Loan Collateral in Kenya

The poorest segment (LSM 1 to 4) shows TV viewership around 24%, while the wealthiest group (LSM 12+) exceeds 90%.

Nairobi and Upper Eastern lead regional viewership, both above 80%. Central also performed strongly at 78%. The lowest figures come from North Western at 67%, revealing considerable infrastructure and access disparities.

Language patterns on TV diverge sharply from radio. A massive 83% of viewers nationally consume content in both English and Swahili, reflecting the bilingual nature of most programming.

Vernacular content maintains regional significance, particularly strong in Central, Lake, Lower Eastern, and Upper Eastern, but represents a much smaller share than on radio. Purely English or purely Swahili content rarely exceeds 10% viewership anywhere.

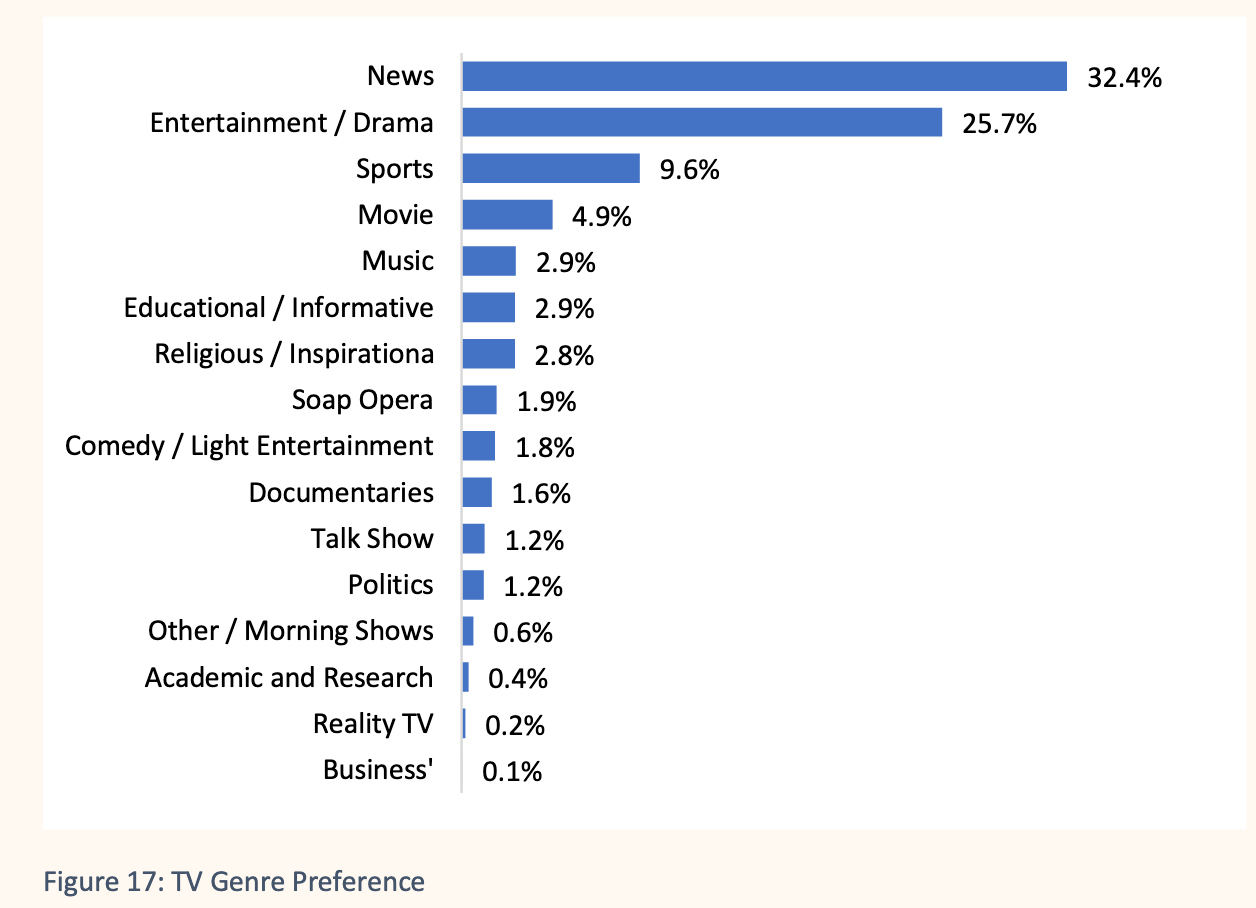

News leads TV content preferences at 32.4%, followed by entertainment and drama at 25.7%. Sports captures 9.6%, while movies take 4.9%.

The Reality of Pay TV

It should come as no surprise that free-to-air television dominates Kenya’s broadcasting landscape. About 84% of viewers watch FTA channels compared to just 16% accessing pay TV.

This split holds steady across gender, though younger audiences aged 18-24 show slightly higher pay TV access at 24%.

Urban residents and wealthier households drive what pay TV market exists. Cities report 24% pay TV reach versus 11% rural. The highest income bracket shows 27% pay TV access, while middle-income groups hover around 17-21%.

READ: MultiChoice To Cut DStv Decoder Prices by 40% to Reboot Pay-TV Strategy in Africa

The lowest income segment barely registers at 14%.

These figures explain why advertising revenue flows overwhelmingly to free-to-air channels. In early 2025, FTA TV captured over KES 3 billion in advertising per month, while pay TV struggled to reach even KES 10 million monthly.

Internet Usage Keeps Rising

Internet usage hit 60% of the population in early 2025, up from 56-57% in previous quarters. The gender gap persists here too, with 65% of men reporting internet access versus 56% of women.

Age determines digital engagement more than any other factor. Youth aged 15-24 show internet usage above 70%, peaking at 75% for the 18-24 group. Usage then declines steadily with age, dropping below 40% for people 45 and older.

Cities show 76% internet access compared to 52% in rural areas. Income creates an even sharper split as the wealthiest segment reaches 92% internet usage, while the poorest manages just 9%.

Nairobi leads internet access at 80%, followed by North Eastern at 76%. South Nyanza records the lowest penetration, highlighting the infrastructure gap.

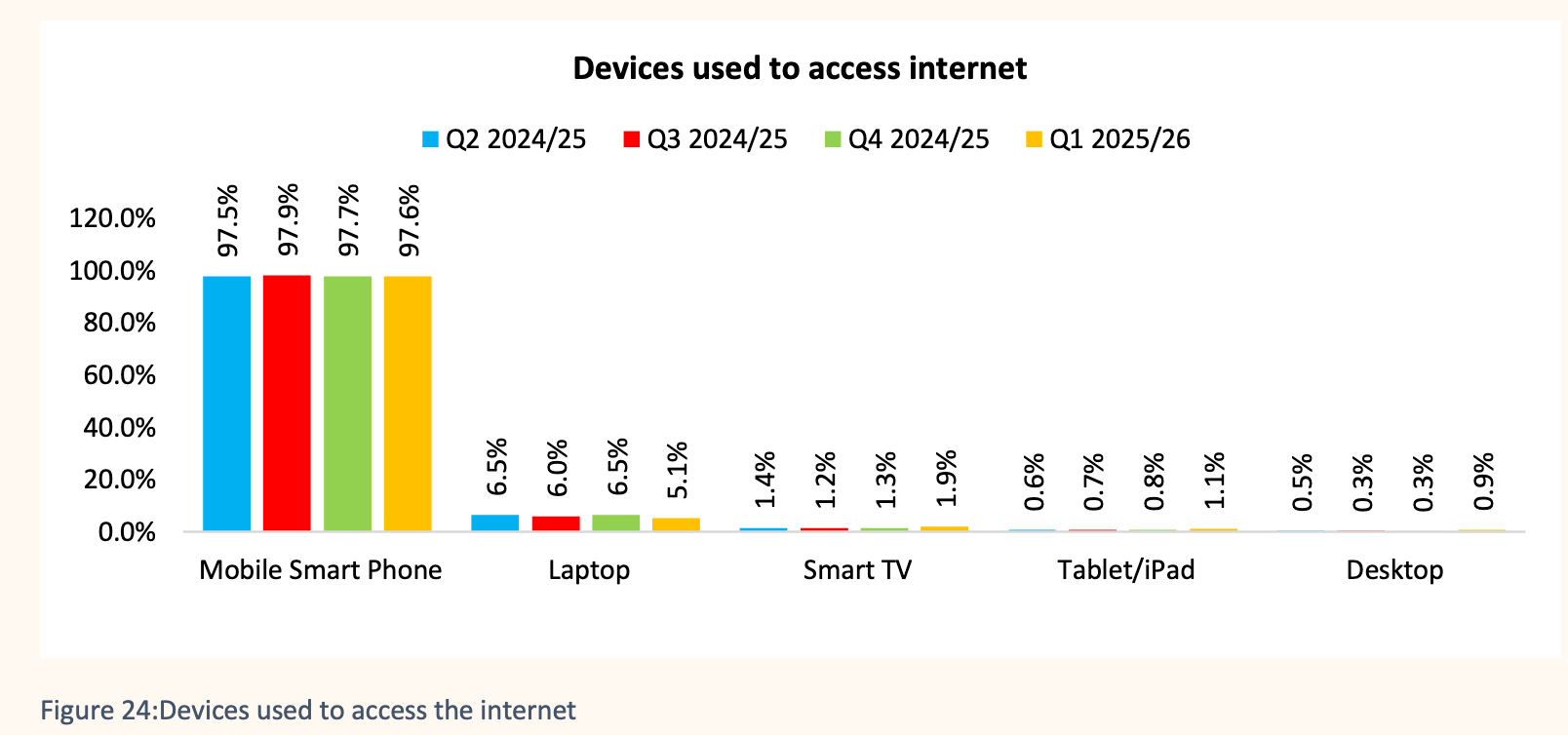

Smartphones drive internet access. About 97.6% of internet users access the web via mobile phones. Laptops trail at just 5.1%, with tablets, desktops, and smart TVs barely registering.

Social Media’s Platform Pecking Order

Facebook and WhatsApp tower over Kenya’s social media landscape. Facebook captures 63.9% usage, while WhatsApp reaches 54.4%. TikTok has surged to third place at 29.5%, followed by YouTube at 26.2%.

Instagram manages 13.3% usage, while Twitter (X) sits at 10.1%. The gap then widens drastically, with Chrome browsers at 6.8%, Telegram at 1.8%, and Opera Mini at 3%. LinkedIn, email, and Snapchat barely register, each under 1%.

Newspapers Keep Struggling

When former president Uhuru Kenyatta said newspapers are for wrapping meat, maybe he wasn’t just being snarky, given how print media shows the weakest performance of traditional channels.

Newspaper readership holds at just 19% nationally, with minimal growth over the past year. Magazine readership sits even lower at 7%.

Men read newspapers far more than women, 23% versus 16% in early 2025. The 25-34 age group shows the strongest engagement at 22%, while the youngest and oldest demographics lag.

Urban areas drive what newspaper market exists, with 23% readership versus 17% rural. The income correlation is extreme, as wealthy households show 38% newspaper readership, while the poorest segment barely reaches 3%.

Lake and Lower Eastern regions lead at 22%, while Coast dropped sharply from 17% to 11% in recent months.

Where the Money Flows

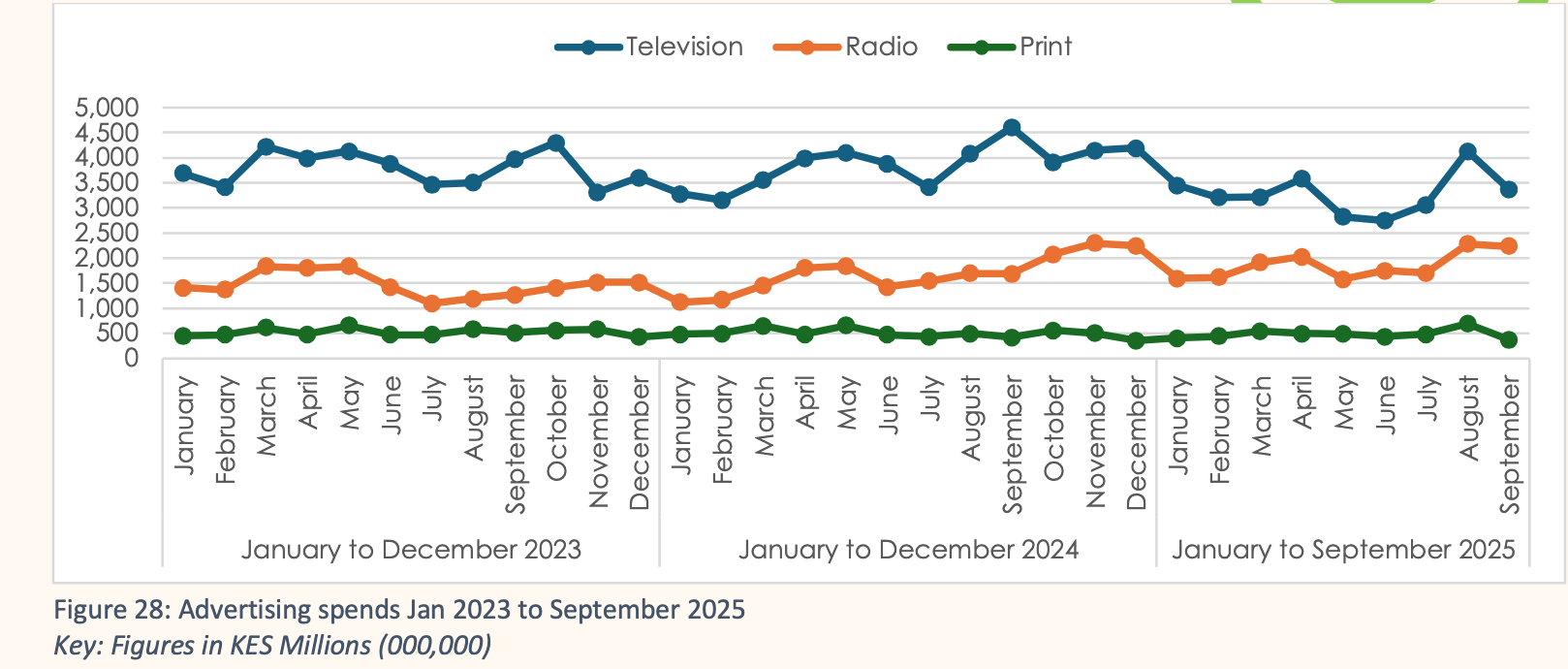

Total advertising spending across radio, TV, and print hit KES 18.3 billion in early 2025, up 15% from the previous quarter. But the distribution reveals clear winners and losers.

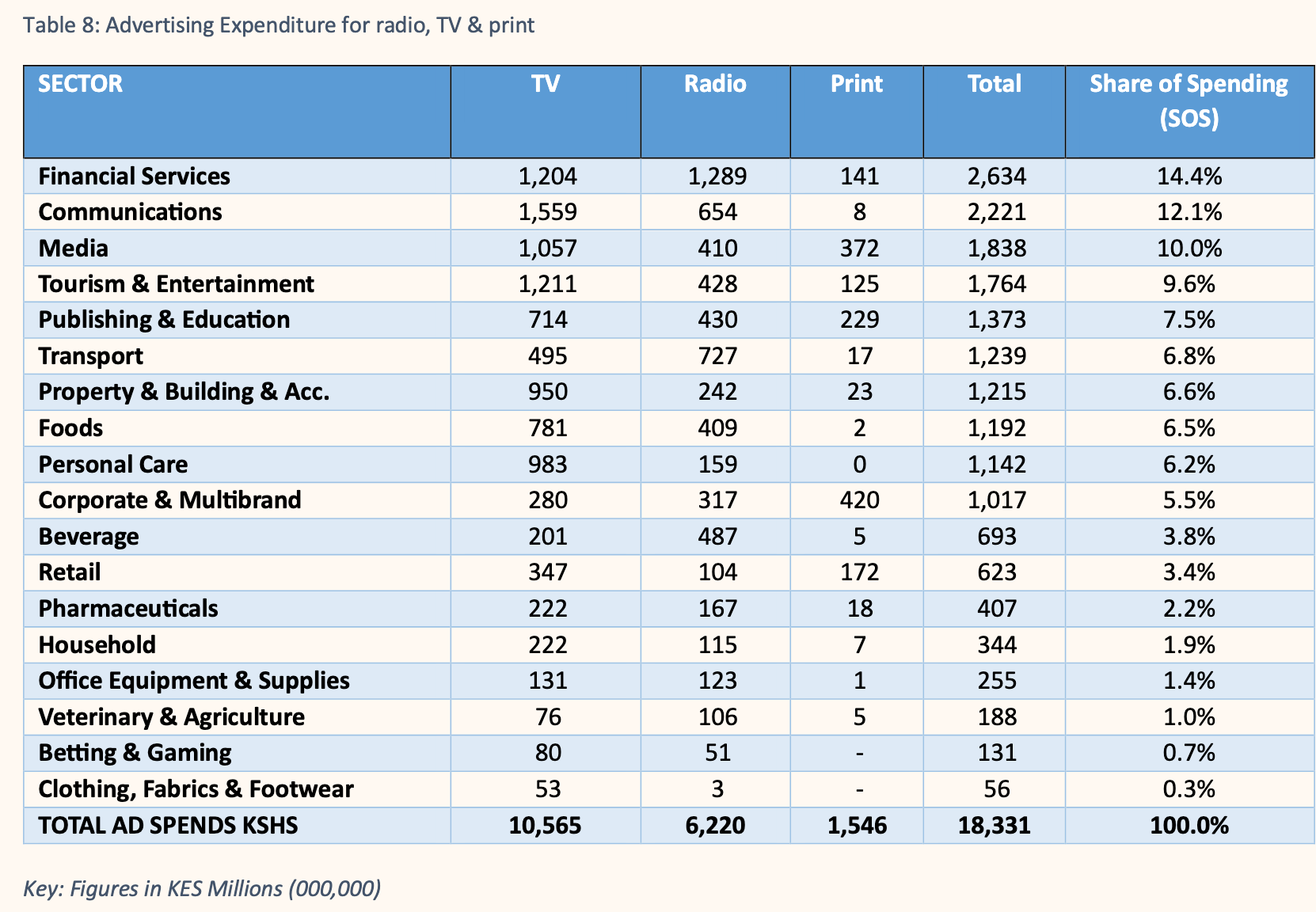

Television captured KES 10.6 billion, with radio taking KES 6.2 billion. Print advertising managed just KES 1.5 billion, showcasing its declining relevance.

Communications led TV advertising at KES 1.56 billion, followed by Tourism & Entertainment and Financial Services, each exceeding KES 1.2 billion. Financial Services dominated radio at KES 1.29 billion, with Transport and Communications following.

Print advertising concentrated heavily on media self-promotion and corporate/multi-brand campaigns, together accounting for most of the limited spending.

Digital advertising tells perhaps the most important story. Brands invested an estimated KES 11.76 billion in digital channels during the same period, rivaling traditional media’s total spend.

Meta platforms (Facebook and Instagram) captured 79% of digital investment. Programmatic display ads took just 9%, with Google Display Network the preferred server.

How This Data Affects Decision Makers

As the data suggests, traditional media still maintains broad reach, especially among older, rural, and lower-income populations. However, younger, urban, wealthier Kenyans increasingly split their time between traditional broadcasts and digital platforms.

Broadcasters can’t ignore that 60% of Kenyans now access the internet, with smartphones making digital content accessible anywhere. Social media platforms, especially Facebook, WhatsApp, and TikTok, command massive daily engagement that competes directly with broadcast programming.

Although traditional media still captures a huge amount of advertising spending, digital’s KES 11.76 billion investment demonstrates where brands see future growth.

The concentration of digital spending on Meta platforms, however, creates its own risks, since it leaves advertisers dependent on foreign-owned networks with algorithmic volatility.

Radio’s resilience stems from its accessibility and local relevance, particularly through vernacular programming that connects deeply with communities.

TV’s strength lies in its combination of broad reach and visual impact, though pay TV’s failure to gain traction clearly limits premium content monetization.

The generational divide poses the clearest threat. As digital-native young people age into prime consumer demographics, broadcasters that fail to meet them on digital platforms risk permanent audience loss. The drop in 18-24 TV viewership from 80% to 72% suggests this shift is already underway.

Kenya’s broadcasting industry isn’t dying, but it is transforming. Businesses looking to be successful will require hybrid strategies that leverage traditional media’s proven reach while building digital presence beyond simple social media pages.

The winners will be broadcasters who understand that in 2026, radio, TV, and digital aren’t competing mediums but complementary channels reaching different segments at different times.

*LSM: Living Standards Measure (classifies standard of living and disposable income)

{kind=link}